Registered card programs as a loyalty marketing enabler are not new. They have been around since the early 2000’s and were primarily the hype of certain credit card issuers and PLCC merchants. The premise sounded good – no loyalty card or special ID required, just use your registered credit card at POS and get your rewards. With payments data already on the network somewhere, if that data were captured and linked to the registered card no special tech integrations and start-up costs were required to tie POS transaction details to a special ID vehicle and back end loyalty management system.

Most of these schemes failed.

By Mike Capizzi

Consumers pay at POS anyway they want; however they wish; and it was extremely foolish to recognize and reward best customers ONLY when they paid for their purchase in a specific manner. Furthermore, not every best customer wanted another card, or that specific card, and were therefore disqualified from participating in a merchant’s loyalty program. Plus, there was always that uneasy feeling about registering your credit card number.

Fast forward to 2018 and we have new systems in place to provide real opportunity for the re-invigoration of registered card techniques.

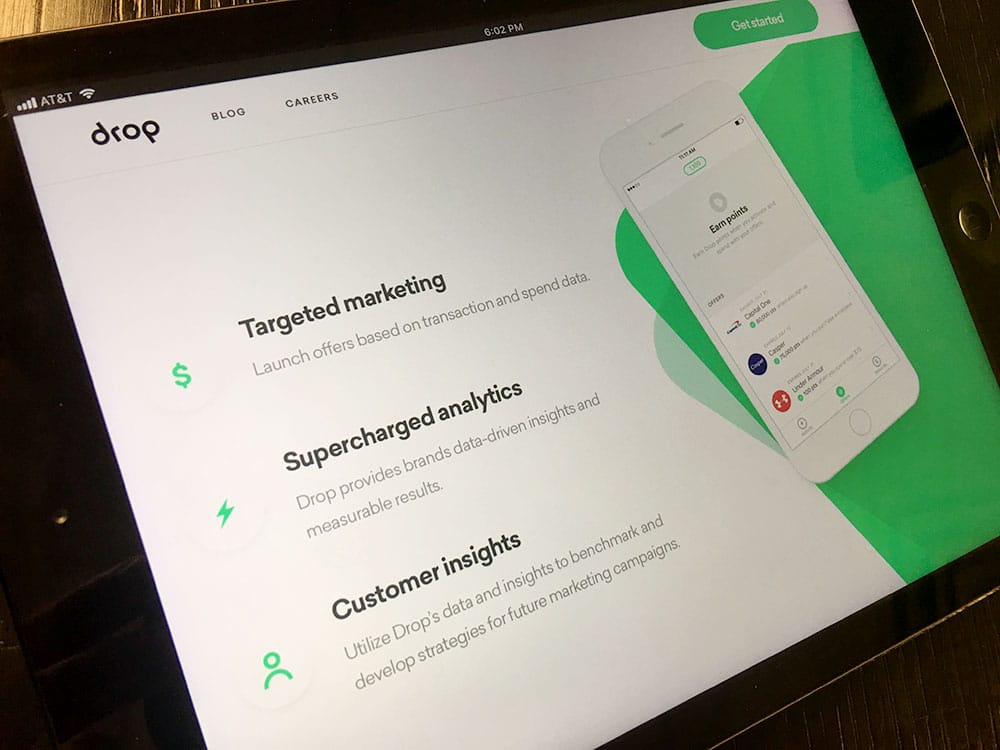

Toronto-based Drop, whose loyalty app allows consumers to collect points for transactions they make and then receive reward offers, has secured a $21 million Series A round led by investors at NEA. The company has previously raised about $5 million in seed capital over the past year.

Drop’s concept is simple. Unlike traditional loyalty and rewards programs which are built around the retail point-of-sale system, Drop uses banking APIs to read your card transaction data directly, and gives you points for making purchases with partners in their program. These points can then be spent on personalized offers, such as a discount on coffee at Starbucks or a free ride on Uber.

Members download the app, register any number of debit or credit cards with the program and earn benefits whenever and wherever they shop within the Drop network of merchants and use any of those cards.

Drop picked up momentum in Canada in 2016-17 and is now poised for growth in the US. Should anybody be paying attention?

At the Wise Marketer we always pay attention. We have been watching Drop for awhile and have reached several important conclusions. First, they totally fit the frictionless model we have been advocating since 2016. Easy to enroll, easy to earn, easy to redeem, no hoops to jump through. Second, this is really a coalition business model with a complete network effect – the consumer benefits at any one of the merchants in the Drop network, not just a single retailer. Offline, on-line, with a large selection of top merchant brands. There is no merchant specific enrollment, just download the app or go to the website or use your mobile phone as the ID device and register your cards. Third, those cards are not limited to single tender types – any number can be linked to your Drop account and both debit and credit can be utilized. Fourth, Drop’s growing popularity stems from early adoption by the millennials and all loyalty practitioners have been chasing this group for some time now, often with little success. Fifth, check out Drop’s management team, their security systems and the new round of venture capital to fund US expansion and you will like what you see.

Drop has reached as high as the second place in the lifestyle category of the Apple App Store, behind Tinder. Derrick Fung, CEO and co-founder, said the two apps are in many ways symmetrical. “We always joke that Tinder allows you to find love, and we allow you to find money,” he said.

The app currently sits in the top five of the U.S. for lifestyle according to AppAnnie data. The company says that it has hit one million users late last year.

Although we have never been a fan of loyalty apps, especially those specific to a single brand (who wants 40 loyalty apps on their phone?), Drop has two distinct advantages to help boost downloads. First, it is network app, not a merchant branded one. Second, it is targeted specifically to a millennial audience that is critical of and less engaging with traditional loyalty program mechanics.

Drop still has a way to go. The website is not very transparent about the earning of benefits and the value prop for the member is a little weak. The burn side is mostly gift cards, but there is a mobile redemption component. Credit earns more benefits than debit, but we all understand the underlying economics behind each payments model and are glad both are acceptable. Merchants who still have a significant amount of cash transactions will not be able to reap the true benefits of the Drop model. We did notice some use of bonuses – invitation/enrollment bonuses, some added points for non-card behaviors and extra credits for taking the brand’s own app.

Like all coalition models the key will be the network – especially the US build out. The company has set internal goals of reaching 5% of the millennial market within 12-18 months, and then 10% of the market within two years.

We wish them luck and will continue to watch as they unfold.

Mike Capizzi is a Certified Loyalty Marketing Professional (CLMP) and Dean of the Loyalty Academy.