Loyalty marketing has its own language. If you’re contemplating launching a points-based loyalty program for the first time, you’ll be encountering a host of esoteric financial terms and concepts specific to loyalty marketing. It’s important that you understand and master each one.

We are pleased to share this new thinking from two recognized voices at Maritz Motivation Solutions on the topic. Many thanks to the authors for their great thinking and insight.

By: Barry Kirk, CLMP, VP Loyalty Solutions, Maritz Motivation Solutions & JR Slubowski, Senior Director Marketing Strategy and Consulting, Maritz Motivation Solutions.

At the most basic level, the financial aspects surrounding a new loyalty program will predominately be associated with point liability. This term refers to a “holding” account for earned program currency that is outstanding and expected to be redeemed at some future point. We use the term “point” to represent any currency earned as part of a loyalty program that can later be redeemed for something of value. Points reserved within the liability account are converted into a dollar amount and reside on your organization’s balance sheet.

Point liability is essentially an obligation or a debt owed on the part of a company. It represents a payout, in points, that is owed to members and may be demanded at some point through redemption.

Many factors can affect point liability and the overall financial health of your program. Learning how to expertly manage these concepts takes time and experience, but you can get a head start by learning these five keys financial realities of loyalty marketing:

[dropshadowbox align="center" effect="lifted-both" width="80%" height="" background_color="#ffffff" border_width="1" border_color="#dddddd" ]1. Rewards expense is incurred when points are issued, not when points are redeemed.[/dropshadowbox]

In most marketing initiatives, accruing for long-term future obligations is not common. In points-based loyalty programs, it’s a daily reality. Because this can be a foreign concept for many marketers, there is a common misconception that redemption creates the expense in a program. In actuality, it is the issuance of points that creates the expense. Since loyalty programs are “evergreen” marketing strategies (at minimum they are a multi-year commitment between the brand and its customers), it’s important to be aware of the accounting liability and accrual rules associated with these programs.

In the accounting world, there is a concept called the matching principle or the Revenue & Expense Recognition Policy. Basically, what this means is that when you recognize revenue in a business, you must also recognize costs associated with acquiring those revenues. In loyalty programs, the points issued to consumers are strongly correlated to the purchases made, such as 1 point for every $1 spent. In fact, the loyalty program points may have helped encourage the customers’ purchases. Therefore, the points must be expensed, or accrued, at the same time the related sale or purchase is made.

Issued points reside in a balance sheet account. This is commonly referred to as point liability or point accrual. This concept is similar to other kinds of obligations or debts that a business may have and that eventually must be paid. In the case of loyalty programs, the obligation will be paid when the consumers redeem or make a claim for their rewards. What makes point liability more complicated than a normal debt or company obligation is that consumers can redeem whenever they choose – today, tomorrow or even three years from now, so long as those points are available subject to any expiration rules (more on that later). In a mature program, you can establish analytical models that effectively predict when points will be redeemed, by whom and at what quantities. However, a newer program will lack the data to support such a model, so you will need to be more conservative in how you assess and handle your potential liability.

Once consumers do redeem for a reward, those points are removed from the point liability or accrual account. This is referred to as liability reduction. It simply means the rate at which consumers are redeeming their points and removing them from liability.

[dropshadowbox align="center" effect="lifted-both" width="80%" height="" background_color="#ffffff" border_width="1" border_color="#dddddd" ]2. In the healthiest of loyalty programs, nearly a third of all points will go unredeemed.[/dropshadowbox]

Another common loyalty concept is breakage. Breakage is closely linked to point liability. Points that “break” are those that will never be redeemed, either because of expiration rules you established or because of member forfeitures. From the consumer point of view, these are points that are intentionally or unintentionally left on the table.

Your financial team will like breakage because it means that a part of the obligation for your program’s points will never get paid out, similar to a debt being forgiven. However, marketers shouldn’t necessarily like breakage because it may be a sign that program members are unengaged and not experiencing the full value of the program.

Breakage varies among different types of loyalty programs, but as a rule of thumb, anywhere from 25-35% of points breaking is considered healthy and a good balance between accounting and marketing objectives.

You can exert some control over breakage through the business rules you set for your program. For example, a 2-year expiration policy will drive higher breakage than a 3-year expiration policy. Or, a program requiring a higher minimum point threshold for redemption will experience higher breakage than one requiring a lower threshold for redemption.

Finally, breakage percentages vary by the engagement level of members in the program. Highly engaged customers that spend the most with your brand are less likely to leave their points on the table. Those that are less engaged are more likely to forget about points or never even achieve the first threshold for reward redemption.

[dropshadowbox align="center" effect="lifted-both" width="80%" height="" background_color="#ffffff" border_width="1" border_color="#dddddd" ]3. There are a variety of ways to handle point expiration, but be careful about a “No Expiration” policy.[/dropshadowbox]

Program policies on expiration vary widely, from no expiration to expiration after just one year or even six months to more creative ways, where expiration is based on activity of the customer. Most loyalty programs build in expiration rules for accounting reasons. If it were up to consumers, they would prefer that points never expire. However, by establishing a definition associated to the life of your points, it will be easier for your finance team to know when to retire outstanding points by removing them from the books and to assess breakage percentages for point liability purposes. That is why it is always recommended that your finance team be involved in the process when you are establishing point expiration rules for your program.

It is worth noting that some loyalty programs have opted not to expire points. This is usually done as a marketing initiative to help acquire program members or as a perk given to high-status members. But if your program is structured so that points never expire, you may be required to keep those points on your books for an indefinite period since they never reach the end of their life and break. This approach can tie up valuable marketing dollars that end up merely sitting in an accrual account on the books. In this situation, points can still break, but the justification is much more difficult and often requires years of data to properly estimate the probability that the points, even without an expiration date, will never be redeemed.

[dropshadowbox align="center" effect="lifted-both" width="80%" height="" background_color="#ffffff" border_width="1" border_color="#dddddd" ]When it comes to point expiration policies, there are three standard approaches you can consider:[/dropshadowbox]

- Fixed Date: This is the most common point expiration structure in loyalty programs. In this model, points expire at a specific date each year, usually three to five years from their issuance date. The fixed date tends to be December 31st for most credit card and hospitality programs. For example, if points were issued on March 1 2018 with a three-year life, they would expire on December 31 2021. This is one of the simpler rules structures, requires minimal programming and accounting procedure. It is also a concept that most consumers understand and accept.

- Period of Time from Issuance Date (Rolling): With this approach, points expire at the end of a period of time, such as three years, from their issuance date. For example, if points were issued on March 1, 2018, with a three-year life, they would expire on March 1, 2021. This rule structure is more common among retail and packaged goods loyalty programs. It is slightly more complicated than “fixed date” and does require more complex programming and accounting procedure. It is not necessarily a difficult concept for most loyalty program members to grasp, but it may create some negativity if members feel surprised when points expire at different times throughout the year.

- Account Inactivity: This approach is typically an “add-on” rule to one of the structures discussed above rather than a stand-alone structure. Here points expire for an individual account when there has been a pre-defined and successive period of inactivity. For example, you may wish to set a 12-month inactivity trigger. Then if points with a three-year life were issued to a member in March 2018, but that member subsequently does not have additional purchases or activity in the next 12 months, those points will expire in March 2019. This rule has become much more common is recent years and is basically a strategy to attempt to re-engage lapsed members, or to eliminate point liability on members that have already left the program. It’s also quite common in airline and other hospitality programs.

If you do decide to go with a “no expiration” policy, we recommend limiting this benefit only to your high-value customers. As your best customers will most likely redeem 90-100% of their points anyway, this strategy will only have a minimal financial impact to your ongoing point accrual.

[dropshadowbox align="center" effect="lifted-both" width="80%" height="" background_color="#ffffff" border_width="1" border_color="#dddddd" ]4. Points are most likely to be redeemed in their second year of life and much less so in their first year.[/dropshadowbox]

Once points are issued, they can be redeemed by members at any time during their life and up until expiration. By analyzing the results of many mature loyalty programs, Maritz Loyalty has found that member redemption patterns tend to follow a predictable trend, one tied back to when points were issued and what their likelihood is to be redeemed at each year of life.

When points are issued, only 5 to 15% of them are likely to be redeemed within the first year. This is usually due to the fact the most members are accumulating points and may or may not have achieved the first level for reward redemption. Obviously, the highest performing and most engaged members achieve the first reward level the fastest. By design, your program should allow for your best customers to have the opportunity to redeem within the first 3 to 6 months of joining the program even though many of those members may still defer their first redemption to a later date.

The vast majority of points issued are usually redeemed with their second year of life – anywhere from 25 to 40%. Much of this is the result of a significantly greater percentage of members having reached by then the first earning threshold for reward redemption (more engaged members may also achieve even higher levels for redemption).

When points reach a life of four or more years, their likelihood of being redeemed starts to diminish. If points are being redeemed in Years 4 and 5, they are most likely issued to 1) less-engaged members who have finally reached the first level of redemption, or 2) to highly-engaged members who have finally accumulated enough points to redeem for a high-value aspirational reward.

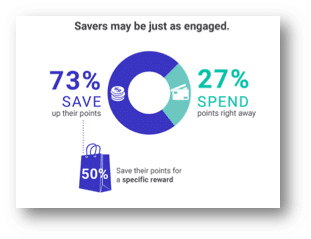

In fact, it’s critical to continuously monitor patterns in redemption behavior as markets do shift. In the most recent Maritz | Wise Marketer Loyalty Landscape report, we learned that 73% of customers actually save points to redeem later for a larger reward. So models may need to be adjusted to reflect more redemption on the later years in the life of a point.

[dropshadowbox align="center" effect="lifted-both" width="80%" height="" background_color="#ffffff" border_width="1" border_color="#dddddd" ]5. Managing point liability costs comes down to four factors: issuance, redemption, breakage and cost-per-point.[/dropshadowbox]

Although companies will vary on the mechanics of accounting for loyalty program points on their books, your approach should include four core factors that will influence you point Liability and accrual:

- Issuance: Obviously, the number of points issued in a loyalty program has a direct impact on the point Liability and accrual expense. The amount of points being issued depends upon the volume of members in the program and the activities for which they are being rewarded.In most loyalty programs, the majority of points are issued for revenue-generating activities like customer purchases and referral. Bonus points may be issued to encourage incremental purchases or to try new products.

However, in a growing number of programs, points are also issued for non-revenue generating activities such as signing up for emails, recognition of birthdays and membership anniversaries, completing surveys or posting on social channels. We typically call these engagement points or “soft points” and they can be a useful strategy for creating a more relationship-based program.

It’s important to understand the financial implications of issuing points and to maintain an annual budget. If your point liability is getting too high, you may need to consider pulling back on point issuance activities -- particularly for engagement activities -- or even establish annual caps on the amount of points earned by members.

- Redemption: Redemption is the act of eliminating or removing points from your point liability. In reality, these points have already been accrued and/or expensed and some may have hit your accrual expense three or more years ago. It is important to note that redemption does indeed reduce point liability. It only impacts the program’s expense if the expected breakage built into the accrual needs to be changed.

In other words, if the percentage of points redeemed is higher than expected, the breakage percentage will be adjusted down and eventually increase both your accrual and point Liability. If the percent of points redeemed is lower than expected, the breakage percentage should be adjusted up and decrease both the accrual and point liability.

Even if the expected breakage built into the accrual is on target and the redemption will have zero impact on program costs, many programs still choose to reduce their point liability. This is because doing so makes your balance sheet look stronger. If you think of point liability as debt on the books, it then makes sense to reduce that debt quickly and make the financial state of the company look more stable.

- Breakage: Breakage refers to the percentage of points that are issued but are never expected to be redeemed, either through expiration rules or member forfeitures. It used to be that you needed to formally cancel out of loyalty programs; today however, most breakage is as a result of “silent attrition.” Customers simply disengage, and it rare to see high percentages of hard forfeitures (the exception is credit cards, but this is because the loyalty program is often as much a part of the card product as the card is).

Normally, the points expected to break are not included in the point liability and accrual expense. Therefore, a higher expected breakage percentage translates to a lower accrual expense. A lower breakage percentage means a higher accrual expense.

Maritz recommends you continuously monitor the points that are being redeemed in your program and re-assess breakage percentage estimates on a periodic basis. For example, if activity and trending analysis shows that more members are leaving points on the table, it’s possible you may be over-accruing expenses. Of course, if that analysis shows more members are becoming highly engaged and redeeming more frequently, you may be under-accruing. In either case, an accounting entry can be made to either increase or reduce the point liability and accrual.

- Cost per Point: Cost per point (CPP) is a simple calculation that represents the value of each issued point and accrued. For example, if 500 points gets a member an item worth $50, each point is worth 1 penny ($50 reward value / 500 points). However, this represents the perceived value to the member, and is most likely not the actual cost of each point from your company’s perspective. In the United States, companies can utilize actual costs when calculating cost per point. But perceived value is the recommended accounting practice internationally.

CPP can be influenced in a variety of ways, but you should be careful not to lower your CPP so much that it impacts the attractiveness of the overall program value prop. One of the most effective approaches to lowering CPP without negatively impacting engagement is to widen the gap between the perceived value to the member and actual cost of rewards to you. The types of rewards offered in your program along with the reward mix offered to different tiers of members plays an important role in that strategy and it is generally helpful to seek out the expertise of a rewards specialist to help you design this approach for a new program.

Finally, don’t let these financial necessities take the excitement out of creating a compelling loyalty program for your company. Your program needs a strong financial foundation to survive, but to flourish it also needs a strong marketing strategy built on a desire for a relationship with your best customers.

Barry Kirk is Vice President, Customer Loyalty Strategy and JR Slubowski is Senior Director, Loyalty Strategy at Maritz Loyalty.