Having spent the best part of a decade working with F&B Operators and their Service Providers here in the UK, I believe the pace of change for how restaurants manage their customers has never been greater. Customers demand seamless, and increasingly digital experiences, that fit around their lives. So, what does this mean for the Food & Beverage sector?

I have highlighted what I see are the four key consumer trends within the sector. Given the current speed of change I will watch with interest which, if any, of these future scenarios will come to fruition in 2019.

Future trends:

- Changes at the ‘point of the customer funnel’ for restaurant discovery, reservations & payments

- Continual growth in restaurant to consumer delivery services

- Disappearance in the previously clear distinctions between drinks manufacturers, distributors, and F&B operators

- Customised food experience based around allergies, ingredients, providence, discovery & preference

What are the scenarios for each of these future trends?

-

-

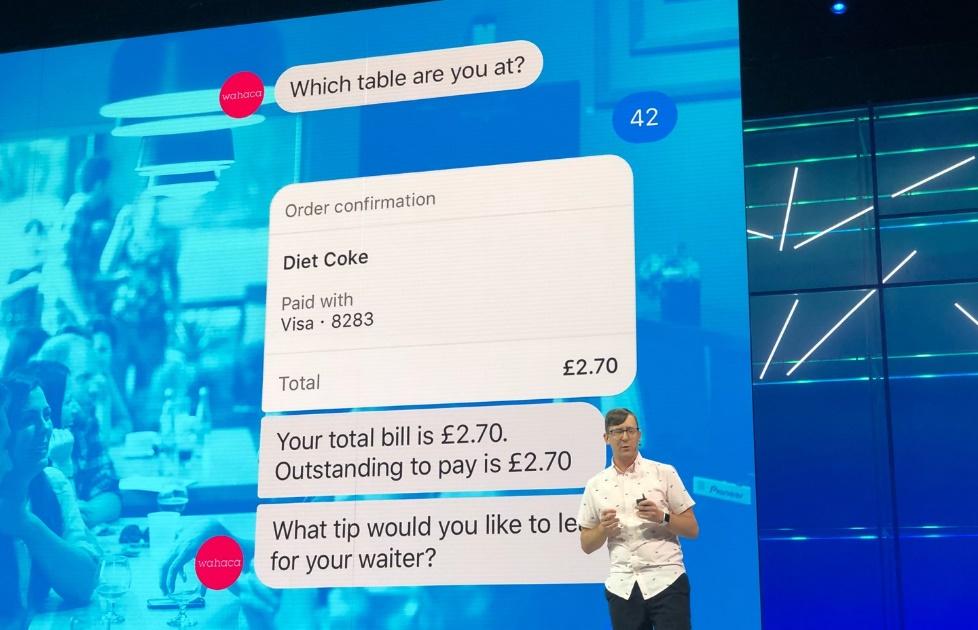

- Traditionally, Instagram & Facebook are not thought of as channels where ‘action happens’ whether making a reservation or paying for a meal. This is changing as Facebook and Amazon allow developers to innovate and trial ‘in location’ payment through Facebook Messenger & Alexa voice command services. Here in the UK, a national burger chain has recently launched an alternative payment option through Facebook Messenger. Rather than installing a branded app or opening a browser guests can now settle their bill directly through their Messenger payment bot. For reservations, a service like OpenTable was previously at the top of the customer funnel. Now it is Google Maps, especially in a city or place which customers are unfamiliar. Just like Retailers before them, restaurant owners now must start considering what their marketing looks like working with the tech giants.

-

- Over the past decade, the UK takeaway delivery market has grown from £2.4 billion to a channel worth £4.2 billion as of February 2018. (Source NPD Group). There is still no strong customer loyalty for any of the leading food delivery apps. However, in taking over control of order transactions, Deliveroo, UberEats’ & Just Eats are also taking ownership over key customer information: address details, payments, demographics, order frequency, location, purchase item. By collecting and using this data they are developing their own business models. Deliveroo are the first of the delivery providers planning to make & deliver its’ own food in direct competition to some of the restaurants they currently serve.

-

- Major drinks manufacturers now seek deeper commercial relationships with those bars & restaurants who purchase their products. The forward-thinking ones are already attempting to move away from a transactional selling model to one in which they gain predictive capability in exchange for providing real commercial insights to individual operators. By accessing and utilising market wide transactional data across all their bar & restaurants, manufacturers are in position provide recommendations for menu items, pricing & targeted staff sales incentives.

- Driven by greater government regulation for advertising of food ingredients, operators will look to new technology providers, whose businesses are based on systems connectivity, to adapt their menus, stock ordering & service models. If operators are to deliver faster menu changes, enhanced menu information & associated pricing there needs to be a far more integrated and collaborative approach to the exposure and publishing of the menu information currently held on the Point of Sale.

-

Who is most under threat?

The pace of this change will have the greatest impact on casual dining chains, service providers & drinks manufactures who do not now innovate in response to the rapid structural changes now taking place within the sector.

-

- Those multi-site restaurant chains who continue to invest heavily in their own branded digital services without consideration for developments within the F&B sector being made by the tech giants like google, amazon and Facebook who hold the ‘point of access’ for their customers.

-

- Reservation platforms, Point of Sale providers, payment providers & loyalty programme operators who do not adopt an open and connected approach to the exposure of their data to other providers within the restaurant ecosystem.

-

- Those drinks manufacturers who continue to base their commercial models on volume sales through distributors without gaining an understanding of end customer preferences.

Nick Chambers is Director at Mobile Loyalty Technologies Limited.